[ad_1]

tolgart

Thesis

Tortoise Midstream Energy Fund, Inc (NYSE:NTG) is a closed end fund focused on midstream energy entities. The CEF has traded at very substantial discounts to net asset value after the Covid crisis, discounts which have averaged almost -20%. The reasons behind this trading pattern is the investors’ loss of confidence in the general MLP asset class, compounded by the inherent leverage in the CEF structure.

Because CEFs do not issue or redeem shares daily and the amount of shares is fixed at the IPO level, daily market pricing is determined by supply and demand. This dynamic results in discounts and premiums to NAV. A CEF management team can a eliminate a pervasive discount to NAV for a fund in two ways:

- Outperform the respective asset class / generate very substantial total returns with low risk in order to garner investors’ interest and have the shares bid up

- Undertake some sort of share retirement (either through a tender offer, liquidation, merger into another fund, etc)

Tender Offer

The Tortoise Midstream Energy Fund management team is trying to address the persistent discount to NAV by targeting share retirements via tender offers:

OVERLAND PARK, KS / ACCESSWIRE / August 10, 2022 / Tortoise and the Board of its closed-end funds previously announced its approval of conditional tender offers as part of the discount management program. A Fund would conduct a tender for 5% of the Fund’s outstanding shares of common stock at a price equal to 98% of net asset value if its shares trade at an average discount to NAV of more than 10% during either of the designated measurement periods. The first measurement period for 2022 ended on July 31, 2022 and it has been determined that a tender offer will be executed in each fund. The tender offers are expected to commence on or around October 3, 2022. The Funds will issue a press release announcing the tender offers on the day the tenders commence. The Funds’ portfolio managers, officers and Board of Directors will not tender their shares. The second conditional tender offer measurement period is from August 1, 2022 through July 31, 2023.

What does this announcement tell us?

- Tortoise views a -10% discount as a natural max market price discount to net asset value

- The manager takes an average value of the discount to NAV during the last 12 months to determine if a tender offer is needed

- The fund expects to retire or tender 5% of NTG’s outstanding shares

- The tender price is 98% of NAV, meaning that the fund is expecting to generate a liquidation discount to NAV of only 2%

- Shareholders who successfully tender their shares are expected to make a Profit = discount to NAV – 2%

- If shares were successfully tendered today that profit would be 15% (17%-2%=15%)

- The tender offer commences on October 3, 2022

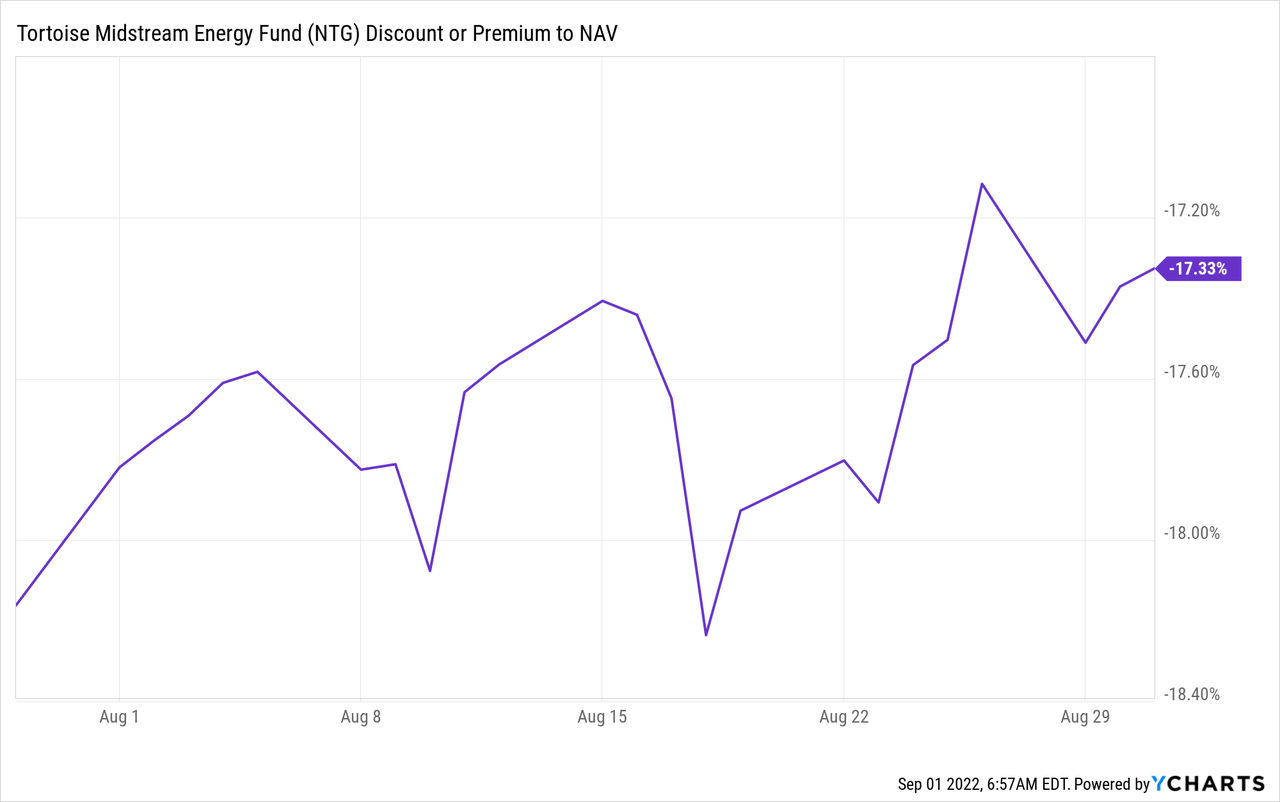

Market Action

The market did not really react into the announcement:

We can see from the above chart that the discount to NAV barely budged, narrowing by just 1%.

We expect this to change going into the tender offer. Nothing is really happening until then. If you are a holder of record of the fund’s shares on October 3, 2022 you will get a notification that you can tender your shares. It is not guaranteed your shares will be successfully tendered, but we expect nonetheless the discount to NAV to narrow on the back of the corporate action.

Risks

If an investor chooses to make a tender offer play on NTG they need to remember they will be long NTG and are betting on the discount to NAV narrowing on the back of the tender offer and potentially a slice of their shares to be successfully tendered. Even if the 5% slice is tendered at a substantial profit, that still leaves 95% of the risk on the books. The investor thus needs to be comfortable with MLP risk, and should be pro-actively looking to onboard this kind of exposure. The tender offer is just an additional positive kick for this type of risk.

Conclusion

Investors looking to enter the midstream energy space should consider making a play on the upcoming NTG tender offer. NTG is a midstream energy CEF that has traded at substantial discounts to NAV since 2020. The fund is tendering 5% of its shares on October 3, 2022 at a price of 98% of NAV versus the current market price of 83% of NAV (current discount is 17%). We expect a narrowing of the discount around the tender date. The investor would nonetheless run full market risk on the underlying assets going forward.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.