[ad_1]

marchmeena29/iStock via Getty Images

Thesis

The Barings Global Short Duration High Yield Fund’s (NYSE:BGH) primary objective is a high level of current income, with capital appreciation as a secondary investment objective.

The vehicle has the “Short Duration” syntagm in its name and indeed it delivers on that aspect via its mandate:

The Fund will seek to maintain a weighted average portfolio duration of 3 years or less

The fund exhibits currently a 2.7 years duration, and on a first look basis, an investor would think it would represent a “safer” fixed income CEF in a rising rates environment. The issue with this fund lies in its collateral composition – the fund has more than 40% of its holdings allocated to “CCC” credits, the riskiest from the capital structure. This has translated into an underperformance for the fund in 2022 on the back of a significant widening in credit spreads.

The vehicle is well diversified and exposes a granular build, but it cannot escape its very credit risky composition. This makes the fund a cyclical one, with substantial losses to be incurred during recessions and large gains to be had upon emergence into recoveries. Its total return profile is reflective of that feature as well, its five-year total return is now negative. The fund is susceptible to actual impairments if this recession is prolonged and deep.

We are not out of the woods yet with the current credit cycle, and while the fund mathematically will not suffer much from even higher rates, its collateral can be significantly impaired if higher rates for longer result in a high wave of bankruptcies. We are on Hold for this name at the moment, but feel the fund’s name does not entirely convey its return profile.

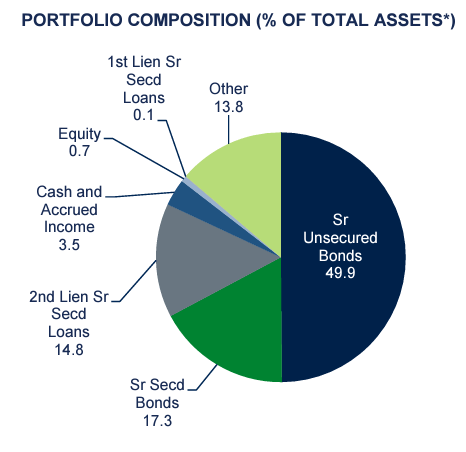

Holdings

The fund invests in a mix of bonds and loans:

Portfolio (Fund Fact Sheet)

We can see that almost 50% of the fund is allocated towards debentures, while 17% goes to senior secured bonds (higher recovery in the case of a default) and the rest towards loans. It is interesting to note the large allocation to “2nd Lien Sr Secured Loans”, which sit below the 1st Lien loans in a capital structure. That translates into much riskier credit profiles for these loans with very low recovery rates in case of bankruptcies.

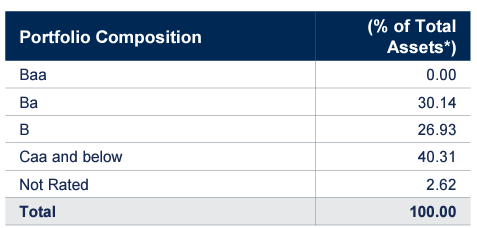

What differentiates this fund is the credit rating profile for the underlying assets:

Portfolio Composition (Fund Fact Sheet)

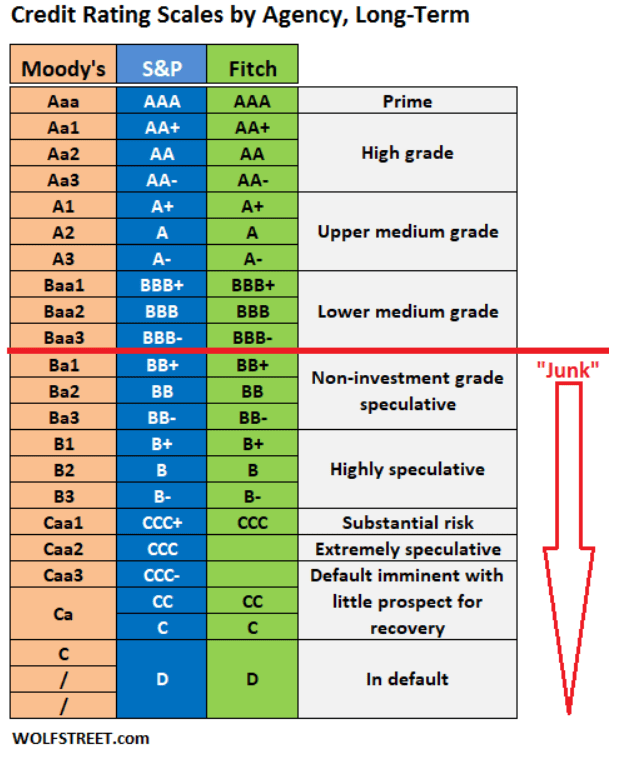

As we can see from the above table, more than 40% of the portfolio is allocated to “Caa” credits, the riskiest ones in a capital structure. Another 26% sits in the second riskiest category, namely the “B” names. As a quick reminder here is how credit ratings work:

Credit Rating Scale (WolfStreet.com)

The higher the allocation to names towards the bottom of the matrix, the higher the risk.

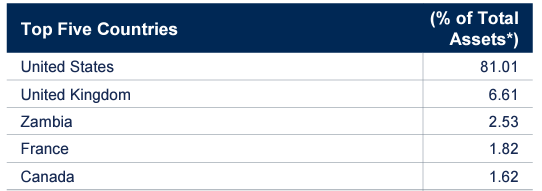

The fund is a global allocation vehicle, but the majority of risk concentration resides in the US:

Top Countries (Fund Fact Sheet)

Global funds tend to be underperformers due to the geopolitical idiosyncratic risks that are very hard to price by financial markets. A perfect example is represented by Russian energy producers. While fundamentally and operationally sound, their debentures took a bath in terms of price action upon the development of the Russia/Ukraine conflict. This aspect cannot be correctly priced by the financial markets because it represents a political decision that is quasi-unpredictable.

Usually, events like the one above result in a higher risk pricing across the board via wider credit spreads for a certain period of time, but then during prolonged market rallies the market tends to “forget” about the incipient event and downshift back to a neutral political risk pricing.

Performance

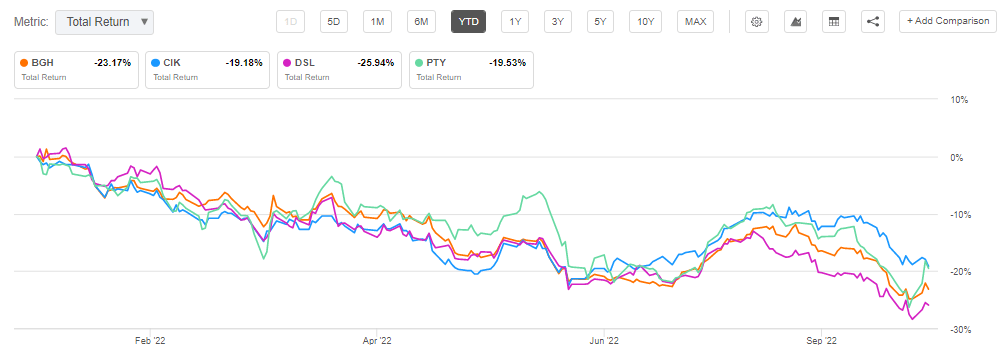

Despite its short duration, the fund has underperformed in 2022:

YTD Returns (Seeking Alpha)

We can see from the above graph that all CEFs in the cohort have somewhat similar performances but BGH finds itself towards the bottom of the performance line. We would have expected more here given the “short duration” attribute. However, the very credit risky nature of the fund drove an underperformance. CCC spreads have blown up this year:

CCC Spreads (The Fed)

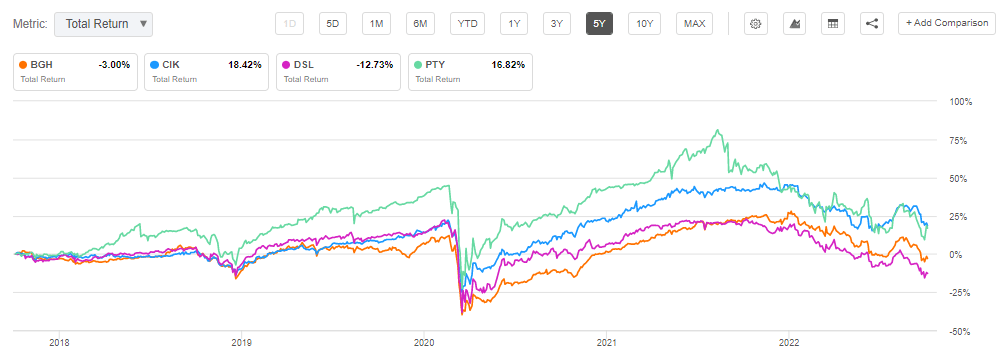

On a 5-year basis BGH is now displaying a negative total return:

5Y Total Return (Seeking Alpha)

This fact makes this fund a very cyclical vehicle. I would not put BGH in the buy-and-hold space because it holds collateral which is too credit risky and the various credit cycle movements ultimately result in long-term underperformance for the fund.

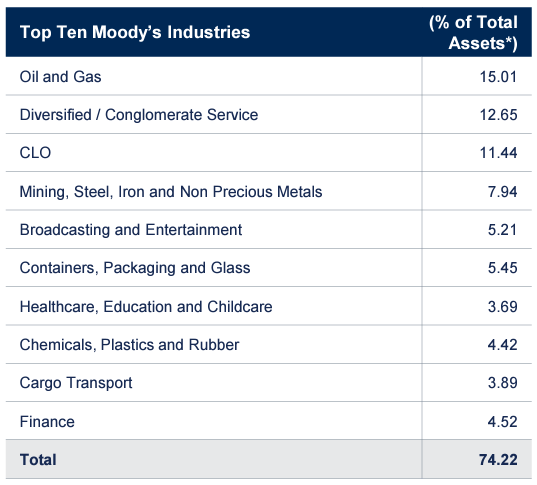

The fund is well diversified from an industry perspective:

Top Industries (Fund Fact Sheet)

We can see that virtually no sector represents more than 15% of the fund, which translates into lower risk for the vehicle.

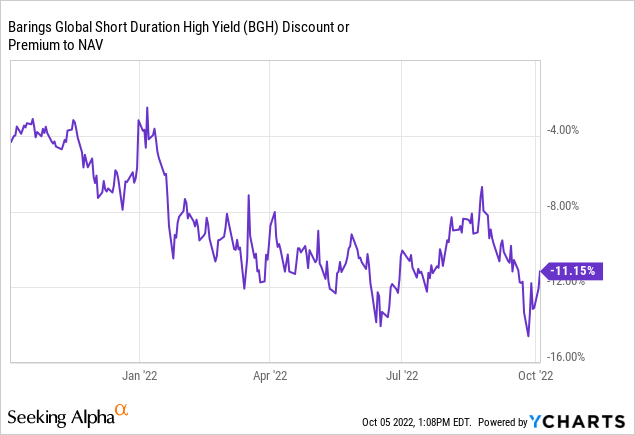

Premium/Discount to NAV

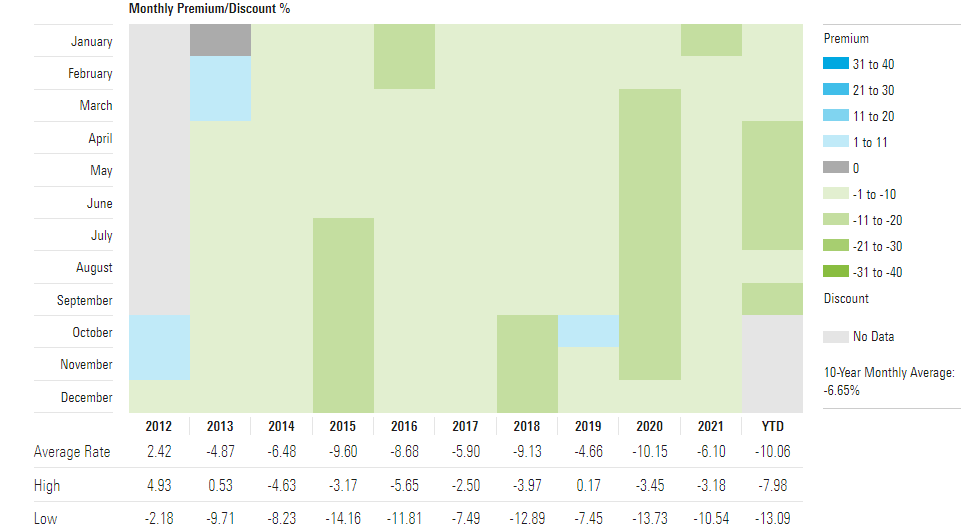

The fund historically trades at a discount to net asset value:

Premium to NAV (Morningstar)

We can see that on average the fund clocks in a -10% discount to net asset value. Looking at this year’s movements the CEF has a classic risk-on/risk-off correlation:

Conclusion

BGH is a fixed income CEF that holds debentures and loans. The fund aims to maintain a portfolio duration below 3 years, which on a first look basis would indicate a less risky vehicle. Upon a closer analysis of the fund’s portfolio, an investor discovers that the vehicle takes significant credit risk via a “CCC” weighted portfolio. The fund has underperformed other CEFs in the space this year due to this feature, despite the savings achieved via a lower duration. BGH is a cyclical fund with deep drawdowns during recessions and the possibility of actual impairments in the portfolio. We are neutral on the name as it stands.

[ad_2]

Image and article originally from seekingalpha.com. Read the original article here.